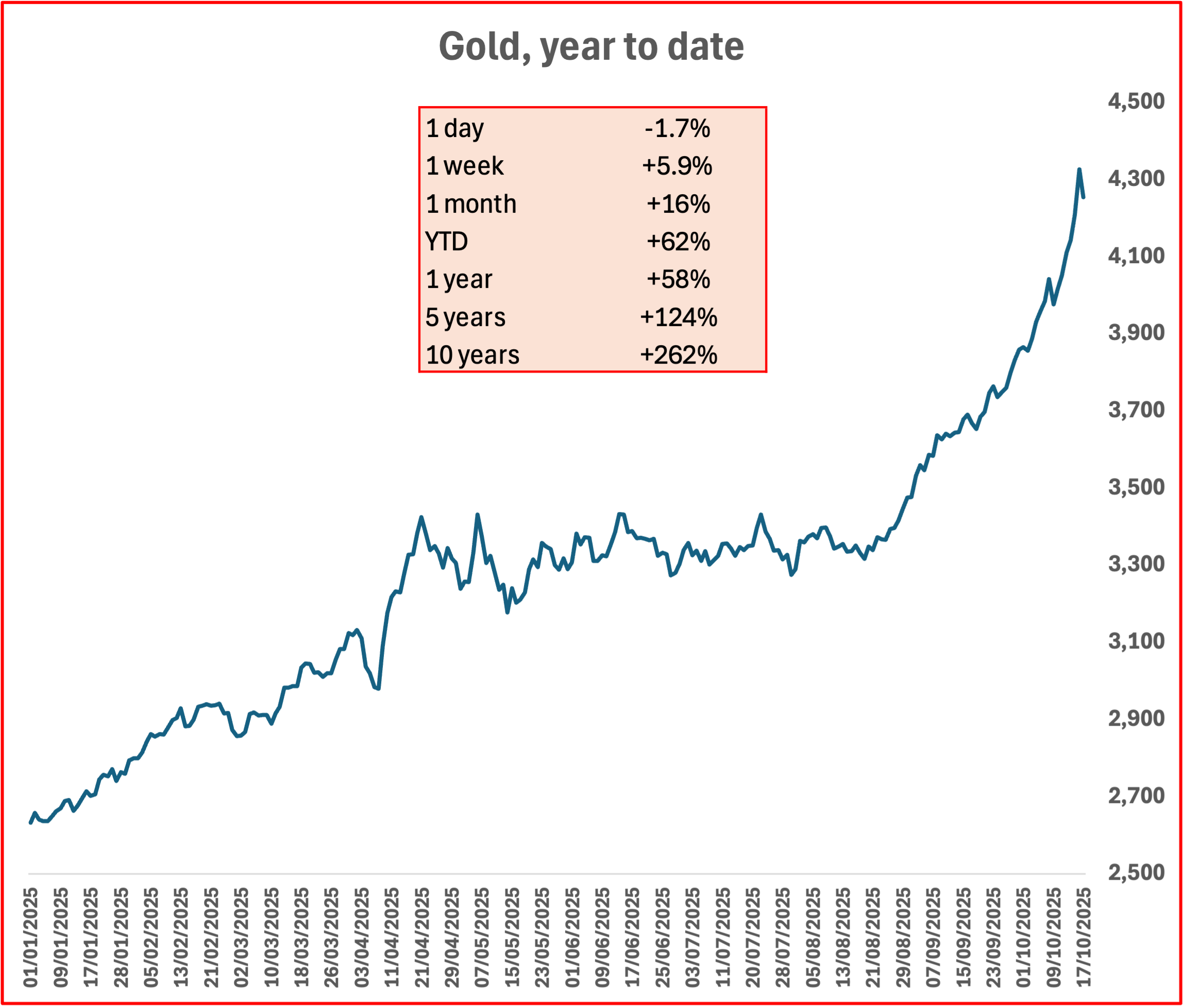

Gold prices have been on a stunning bull run throughout 2025, with the gold price surging nearly 60 percent year-to-date and surpassing $4,300 per troy ounce by mid-October. This dramatic appreciation represents far more than market speculation. Rather, it reflects a profound shift in how the world’s financial institutions manage risk and allocate resources. Understanding the gold price rally requires examining the interconnected forces driving this unprecedented move.

For professional investors accustomed to traditional market dynamics, the most striking aspect of this rally is not merely its magnitude, but the manner in which gold prices have shattered the historical inverse relationship with equities. Throughout 2025, the precious metal has risen alongside equity markets, a phenomenon rarely observed during peacetime economic expansions. This unusual divergence signals something deeper at work beneath the surface of conventional market narratives.

A Historical Perspective on Safe-Haven Demand

Throughout history, gold has served as humanity’s ultimate refuge during periods of uncertainty. During the 1970s stagflation crisis, the metal soared from $35 to over $800 per ounce as investors sought protection from simultaneous inflation and economic stagnation. Following the 2008 financial crisis, central banks and investors alike rediscovered gold’s intrinsic value as the financial system appeared on the brink of collapse.

What distinguishes 2025’s performance is not the absolute price reached, but rather the context in which it has been achieved. Unlike previous periods of turmoil, this bull market has emerged amid relatively stable equity valuations and corporate earnings. This peculiarity underscores a market dynamic that transcends traditional risk-off episodes. Instead, we are witnessing a structural transition in how policymakers and institutional investors view the role of gold in a globally fragmented financial system.

The Confluence of Forces Driving the Rally

Several interconnected dynamics have propelled gold’s ascent throughout 2025. Trade policy uncertainty stands foremost among these factors. Escalating trade tensions and tariff policy have rattled markets, weakened the U.S. dollar from recent highs, and sparked legitimate recession concerns among investors seeking safer harbors for their capital. The unpredictability inherent in current trade negotiations has created an environment where traditional hedging strategies appear inadequate.

Central bank demand has emerged as the most significant structural pillar supporting prices. Over the past several years, central banks have dramatically accelerated their gold accumulation programs, acquiring record amounts as they deliberately diversify away from dollar-dependent reserves. According to J.P. Morgan Research, central banks are expected to purchase approximately 900 tonnes of gold in 2025, continuing a multiyear trend that has reshaped reserve management philosophy.

This shift reflects far more than routine portfolio rebalancing. It represents a deliberate recognition of geopolitical fragmentation and the potential for financial system weaponization. According to some analysts, central banks may for the first time since 1996 collectively hold more gold than U.S. Treasuries, a symbolic milestone that underscores the magnitude of this secular shift in reserve management philosophy. Among major reserve managers, China, India, and Russia have led the charge, with the People’s Bank of China alone increasing its gold reserves significantly in recent quarters.

Geopolitical tensions have simultaneously amplified safe-haven demand. Ongoing conflicts in Ukraine, Middle Eastern hostilities, and escalating U.S.-China trade frictions have created an environment where investors perceive tangible risks to the global financial architecture. Additionally, weakened interest rates and market expectations for further central bank rate cuts have made non-yielding assets like gold more attractive relative to bonds and other income-generating securities.

The Investment Demand Component

Beyond central bank accumulation, institutional investment flows have provided substantial support for prices. According to estimates that include OTC markets, futures, and exchange-traded funds, average gold trading volumes reached $329 billion per day during the first half of 2025, the highest semi-annual figure on record. Notably, SPDR Gold Shares (GLD) and other major gold ETFs saw their largest quarterly inflows since 2020, reflecting renewed retail and institutional interest. This surge in trading activity reflects both hedge fund positioning and significant capital flows as professional investors tactically reposition portfolios toward real assets.

This wave of investment demand carries particular significance because it demonstrates that gold’s rally extends well beyond the actions of reserve managers. Sophisticated investors across pension funds, insurance companies, and family offices have begun recognizing gold’s role as a hedge against currency devaluation, inflation persistence, and systemic financial risk. This broadening base of demand, when combined with central bank accumulation, creates a formidable structural floor beneath prices.

Technical Momentum and Market Structure

Gold prices have broken out decisively above $4,200 per ounce, demolishing previous resistance levels that technical analysts had monitored for years. This breakout suggests that momentum may well persist into the first quarter of 2026. As of mid-October 2025, the psychological $4,000 barrier has transformed into dynamic support, with $4,460 emerging as the next major resistance level. The 200-day moving average has turned decisively bullish, while the Relative Strength Index remains in overbought territory. Rather than signaling an imminent reversal, this overbought condition more accurately reflects the strength of the underlying uptrend and the conviction of institutional buyers.

Real yields have moderated from their 2024 peaks, currently hovering around plus 2 percent, but remain historically elevated compared to the deeply negative yields that characterized 2020 and 2021. Yet with inflation expectations remaining elevated relative to nominal Treasury yields, even these positive real rates offer less appeal relative to gold. This dynamic typically provides a powerful tailwind for extended gold rallies, particularly when investors perceive traditional yield-bearing assets as insufficient compensation for risk. Simultaneously, the U.S. Dollar Index has eased from its 2024 highs, lowering the effective cost of gold for non-U.S. buyers and bolstering international demand from emerging market investors facing currency pressures.

Supply, Demand, and Emerging Channels

While substantial price appreciation has incentivized recycling activity, mine production has been constrained by exploration challenges and permitting delays. Supply constraints are expected to support prices, with approximately a 10 percent rise projected in 2025 year-over-year. At these elevated price levels, jewelry fabrication may face headwinds, but investment demand from institutional sources has more than offset any potential weakness in discretionary consumption.

Beyond institutional channels, retail appetite has surged, particularly in China and India, where investors have increasingly shifted capital away from struggling property and equity markets. Premiums on physical bullion have risen sharply in these regions, reflecting robust local demand that extends well beyond financial market narratives. Meanwhile, emerging vehicles like tokenized gold on blockchain platforms have expanded investor access to the metal, further broadening its reach beyond traditional banking and bullion networks.

This multifaceted demand profile, when combined with central bank accumulation targeting specific reserve levels, has created an environment where structural supply constraints reinforce price support mechanisms. Unlike commodities driven primarily by cyclical industrial demand, gold’s primary supply outlet remains constrained by long-term investment demand and reserve management objectives.

Potential Headwinds and Risk Factors

Despite the compelling bull case, investors should remain cognizant of potential challenges ahead. A protracted period of higher-for-longer interest rate policy by the Federal Reserve could undermine gold’s appeal relative to yields. Similarly, if economic data surprises to the upside and market expectations shift toward monetary tightening rather than accommodation, the investment thesis would require reassessment. Unexpected liquidity tightening or financial market stress could also produce sudden dislocations, though such conditions would likely reinforce gold’s safe-haven properties.

At these historically elevated price levels, competitive dynamics within the jewelry and consumer goods sectors may ultimately constrain demand. However, the substitution effects from price remain modest relative to the structural drivers supporting accumulation by institutional investors and central banks.

The Path Forward

Gold’s remarkable 2025 performance reflects legitimate economic and geopolitical concerns rather than irrational exuberance or speculative excess. While valuations have become stretched relative to certain historical measures, the fundamental drivers remain firmly in place. Central bank buying continues at robust levels, policy uncertainty persists globally, and the structural transition in reserve management appears durable rather than cyclical.

For professional investors navigating uncertain times, gold prices continue to serve a valuable function as a portfolio diversifier. Whether viewed as a hedge against currency devaluation, inflation persistence, or geopolitical shock, the precious metal offers characteristics that remain difficult to replicate through traditional financial assets. As global institutions contend with structural economic transitions and unprecedented policy experimentation, the gold price surge appears likely to persist. The current environment suggests that what began as a cyclical bull market driven by headline concerns has evolved into something more durable: a secular shift in how the world’s financial institutions allocate and protect capital.

The question for institutional investors is not whether to maintain exposure to gold, but rather at what portfolio weighting level such exposure appropriately reflects their risk tolerance and time horizon. In this context, the 2025 bull market represents not an endpoint but rather a waypoint within a longer-term shift in global financial architecture.